USCPA試験の内容が一部変更されます。

2023年12月までの試験は従来通り、FAR・AUD・BEC・REGの4科目です。

2024年1月からの試験は、FAR・AUD・REG・(BAR or ISC or TCP)の4科目となります。

当然ながら各種予備校やブログでの情報もまだまだ少ない状況ですが(2022年12月時点)、AICPAのHPを見てきた結論としては

基本BAR選択、IT関連に詳しい人はISC選択もあり、です。

お時間ある方は是非結論の根拠である以下をご覧ください。

最大の特徴は科目BECの消失及びWC(英作文)がなくなる点です。

BECは大別して「管理会計・ファイナンス・経済学・IT・コーポレートガバナンス」の5分野から構成されています。

AICPAの要綱を見ると管理会計とファイナンスはFARの範囲へ、ITはAUDとISCの範囲へ、コーポレートガバナンスと経済学はBARの範囲へ移行するのでBEC試験対策で培ってきた知識が無駄になるわけではありません。

WC(英作文)は完全になくなることは大半の日本人受験者にとっては朗報でしょう。

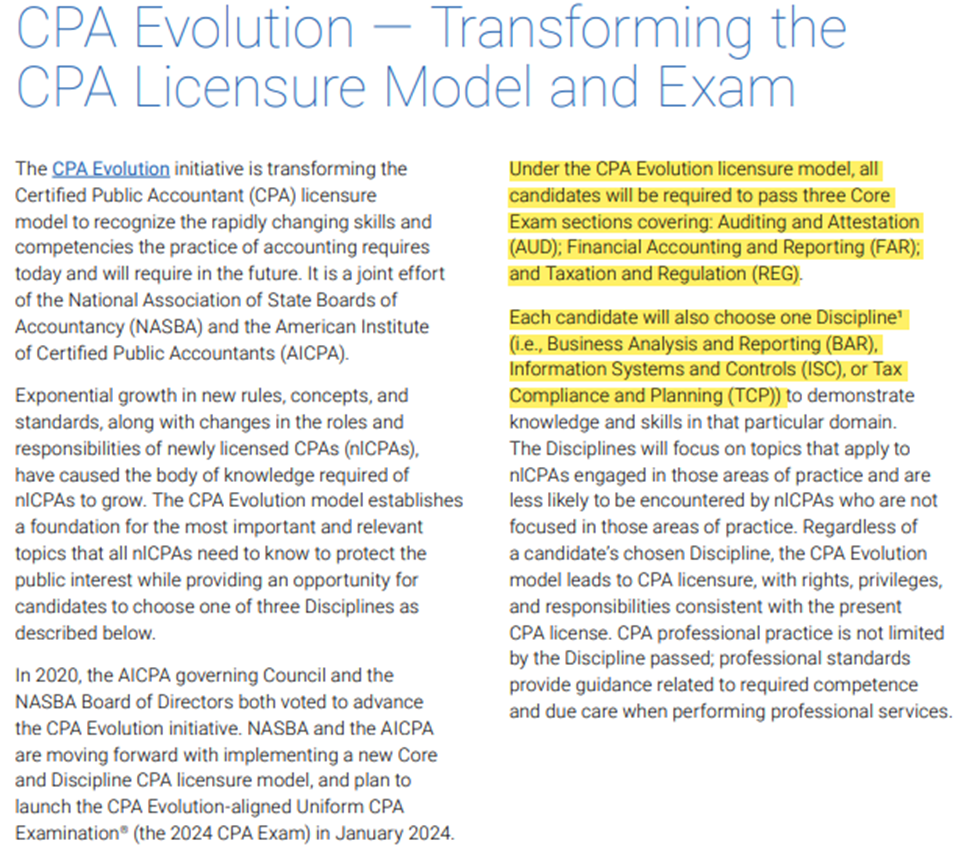

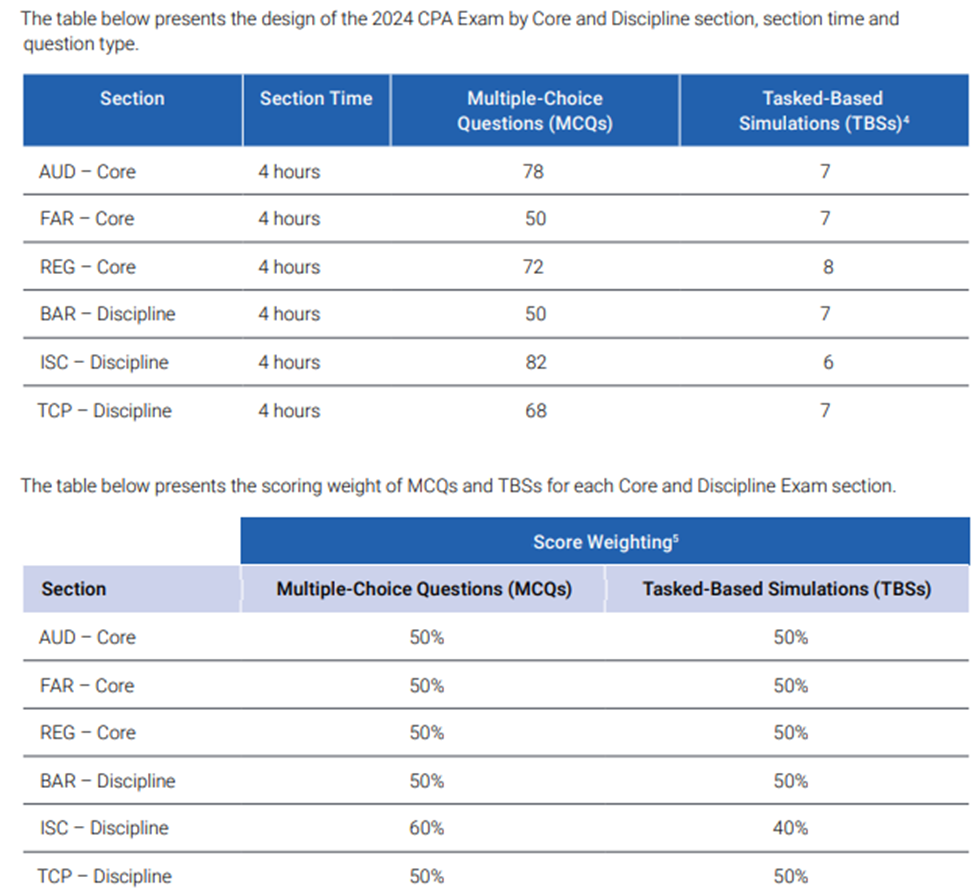

2024年1月からの試験内容目安

以下画像はAICPAのHPから取得しました。

ぱっと見6科目あるように見えますが、Coreが必須科目、Disciplineが選択科目なので4科目の受験となります。

下の表(上から3つ目の画像)にMCとTBSの比率が書かれており、御覧のとおりWCはありません。WCは人間がマニュアル採点していたようなので負担を考慮すると協会にとっても受験者にとってもなくなってくれて負担減ですね。

なぜ試験制度は変わったのか

興味がある方はAICPAのHP記載を見てみてください。

ただ大半の受験者は「そんな暇あったら勉強する」と思います。

私がざっと読んできたので、意訳になりますがまとめます。

①世の中の技術進捗により企業活動や監査がコンピューターシステムに大きく依存している。

②資格取得がより実務に活かせるようにするため

①については監査やってますととても感じます。AUDで言うとSOC1レポートとかですね。

AICPAとしてもSOCレポートに関してかなり注力して出題する事が予想されますのでSOC1とSOC2の違い、SOC3の存在と内容、については把握しておきましょう。

②については当サイトで何回か書いたと思いますが、米国のBig4ではUSCPA試験ってマネージャーへの昇進要件であるケースが多いです。つまりアソシエイト・シニアアソシエイトとして数年監査の実務経験がある人々が受ける試験ですので、当然実務に則した試験内容になりやすい傾向があります。

そして日本の士業試験にも言えますが年々資格保持者の絶対数が増加するので、試験も難化させないと士業の価値が薄まってしまいます。こうした要因も試験の難化理由となっていると思われます。

新科目の内容や難易度

まだ始まってもいないので正確に試験内容を記載することは出来ませんが、AICPAのHPで概要に関する説明がありました。記載内容から所感をまとめていきます。

Business Analysis and Reporting(BAR)

以下英文はAICPAのHP記載内容です。

The BAR Discipline Exam section will test more complex technical accounting topics such as stock compensation, business combinations, and derivatives and hedge accounting. Certain topics will be tested in both the FAR Core Exam section and the BAR Discipline Exam section, such as revenue recognition and lease accounting. For example, the BAR Discipline Exam section will test:

• The analysis and interpretation of agreements, contracts, and other supporting documentation to determine whether revenue was appropriately recognized.

• Recalling and applying lessor accounting requirements and analyzing the provisions of a lease agreement to determine whether a lessee

The BAR Discipline Exam section includes content from BEC on non-financial measures of performance; managerial and cost accounting concepts and the use of variance analysis techniques; budgeting,forecasting, and projection techniques; factors that influence an entity’s capital structure, such as leverage, cost of capital, liquidity, and loan covenants; financial valuation decision models used to compare investment alternatives; risk management topics including the COSO Enterprise Risk Management framework; and the effect of changes in economic conditions and marketinfluences on an entity’s business

赤マーカーがポイントです。

前半部分はFARで登場する科目のうち難易度が高めの内容が多いです。特にデリバティブやヘッジ会計は身近でない分取っつきにくい方も多いでしょう。ただこれらの分野は慣れてしまえば簡単ですのでFAR合格のためにも勉強はおすすめです。

後半はほとんどがBECの管理会計とファイナンス論、コーポレートガバナンスと経済学の範囲となっています。

赤字は新傾向です。オルタナティブ投資の比較に用いるための評価モデルと書かれています。

少なくとも私が勉強を開始した2017年~当記事を書いている2022年12月時点ではUSCPA試験にオルタナティブ投資評価モデル関連の出題された例は把握していません。別ページで書けるぐらいの内容になりますし、各予備校も対応に追われるでしょう。

Information Systems and Controls(ISC)

以下英文はAICPAのHP記載内容です。

The ISC Discipline Exam section tests the knowledge and skills an nlCPA must demonstrate with respect to information technology (IT) audit and advisory services, including SOC engagements.

The ISC Discipline Exam section also tests the knowledge and skills that nlCPAs must demonstrate with respect to data management, including data collection, storage, and usage throughout the data life cycle.

With respect to SOC engagements, the ISC Discipline Exam section primarily focuses on:

• The use of the Description Criteria for a Description of a Service Organization’s System and Trust Services Criteria for Security, Availability, Processing Integrity, Confidentiality, and Privacy in planning, performing, and reporting in a SOC 2® engagement.

• Planning, certain procedures (excluding the testing of internal controls over financial reporting) and reporting on a SOC 1® engagement.

The ISC Discipline Exam section includes content from BEC on certain aspects of business processes and internal control, risks associated with IT and controls that respond to those risks, and data management and relationships.

青マーカーがポイントです。

上述した通り実務で欠かせないSOCレポートに関するIT知識が中心となります。

後は旧BECのIT分野がISCに含まれるという旨が記載されています。

この科目は「ITに強い」「SOCレポートを(実務等で触れていて)よく知っている」受験生にとってはかなり狙い目ですね。

私も監査人としてSOCレポートには沢山触れてきているので当サイトでも別途SOCレポートに関する記事を書く予定です。

Tax Compliance and Planning(TCP)

以下英文はAICPAのHP記載内容です。

The TCP Discipline Exam section tests the knowledge and skills an nlCPA must demonstrate with respect to U.S. federal tax compliance for individuals and entities with a focus on nonroutine and higher complexity transactions, U.S. federal tax planning for individualsand entities, and personal financial planning.

The assessment of federal tax compliance will focus on an nlCPA’s role in both the preparation and review of tax returns.

The assessment of federal tax planning will focus on an nlCPA’s role in determining the taximplications of proposed transactions, available tax alternatives, or business structures.

The assessment of personal financial planning will focus on planning strategies and opportunities that an nlCPA typicallyidentifies in connection with the preparation and review of individual tax returns.

As explained above in the REG Core Exam section, existing REG content will be allocated between the REG Core Exam section and the TCP Discipline Exam section.

The TCP Discipline Exam section will focus on nonroutine and higher complexity tasks, including, for example, consolidated C-Corporation tax returns and international tax issues.

黄色マーカーがポイントです。

個人的にはTCPは避けたいですね…。旧REGの内容を飛び越えていて単純に難化REGという書き方ですし、更には赤字の国際税務に至っては完全に新分野です。

ちなみに日本在住USCPAのメジャーな職場としてBig4等の税理士法人での国際税務(移転価格税制アドバイザリー等)があります。

こういった業務に就いている or 興味がある人はTCP選択でしょうがそれ以外の方がTCPを積極的に選択する必要はないかと思います。

結論:基本BAR選択、得意な人はISC選択

BECで培ってきた管理会計とファイナンス論、コーポレートガバナンスに経済学と4/5分野が活かせるBAR一択だと思います。

BECを全く勉強していない人でも必須科目FARの勉強に比率分析は必要なので結局ファイナンス論は勉強する必要があります。そうした点でもBAR選択をお薦めします。

ただ、「元々BECのITが得意だった」「職業がIT関連で知識に自信がある」「SOCレポートのことなら何でも聞いて」という人はITCの選択もありなのかなという所感です。

【参考】:2024年からのFAR、AUD、REG

Additionally, the Core FAR Exam section will test the foundational concepts related to state and local governments as issued by the Governmental Accounting Standards Board (GASB), including measurement focus, basis of accounting, and determining the appropriate funds in which to record activities. Under the Core and Discipline Model, some existing FAR content will be allocated between the FAR Core Exam section and the BAR Discipline Exam section, for example, revenue recognition and lease accounting. Revenue recognition in the FAR Core Exam section will assess recalling basic concepts of accounting for revenue and applyingthe five-step model to determine the amount and timing of revenue recognition. Lease accounting in the FAR Core Exam section will assess lessee The Core FAR Exam section includes content from BEC related to understanding and applying financial statement ratios and performance metrics

FARについては上記内容から「5 step アプローチ」や「リース会計」といった応用分野はFARにもBARにも出題される、と読み取れます。

FARの学習内容がBARにも登場するので、BAR選択が最もコスパがよさそうです。

In 2021, as a result of the 2020 PA, the AUD section was expanded to emphasize: (i) technology as an external factor in the understanding of the business, (ii) understanding significant business processes and related IT systems, and (iii) identifying and documenting the significant components of an entity’s control environment, including entity level and IT general controls.

AUDはとにかくITを強化すると言っていますね。記載してくれている通りSOCレポートが中心となりそうです。

The REG Core Exam section tests the knowledge and skills that all nlCPAs must demonstrate with respect to U.S. ethics and professional responsibilities related to tax practice, U.S. business law, and U.S. federal tax compliance for individuals and entities with a focus on recurring and routine transactions.Under the CPA Evolution Core and Discipline model, existing REG content will be allocated between the REG Core Exam section and the TCP Discipline Exam section.The REG Core Exam section will focus on routine and recurring tasks and the TCP Discipline Exam section will focus on nonroutine and highercomplexity tasks.For example, the REG Core Exam section will test individual gross income concepts like wages, interest and dividends, guaranteed paymentsreceived from a partnership, and income from a qualified retirement plan, while the TCP Discipline Exam section will test gross income concepts like the exercise of incentive stock options (ISO), imputed interest on a below-market-rate loan, and compensation earned while employed outside the U.S.

REGは旧REGから応用分野をTCPへ移行すると記載されています。単純に範囲が減少し受験者の負担減ですね。